C2V January Notes From The Trenches

Welcome friends! A very happy new year to everyone.

Since we covered the high points of where we think things are headed in our 2026 predictions piece last month, we thought we’d just do a quick roundup of (mostly) timely news items, with an unintetntional concentration in an area we rarely delve into – the EV/mobility space (but don’t worry, we wedged some AI stuff in there too).

Where else would one start in talking about EVs and the latest in mobility innovation…

Tesla’s Sales Stagnation, the “Elon Premium”, and Leaning Into Strengths

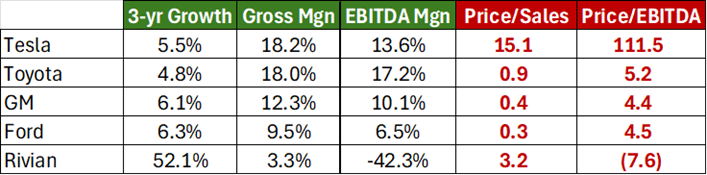

For years, Tesla enjoyed the rare combination of explosive growth (41% annually from 2019 – 2023) and exceptional operating efficiency (gross and EBITDA margins at or well ahead of industry leaders). For years, Tesla has also traded at a truly staggering premium relative to its auto manufacturing peers. While its price-to-sales and price-to-EBITDA multiples were hard to justify even with the exceptional performance, at least there was exceptional performance to point to.

Since 2023, however, growth has ground to a halt (+5.5% annually over the past three years and -0.6% over the past two). Margins have also come in significantly, remaining in the top tier of the industry, but no longer a tier unto themselves and yet, the exceptional premium hasn’t changed at all. In other words, by the numbers, Tesla is an excellent auto company, trading at 2 - 3x the sales multiple of the average high-growth software company.

{kind=link}

Of course, the real justification for this premium has always been the notion held by a large number of people that Elon Musk’s genius is so comprehensively far above that of every other person on earth that they couldn’t afford to miss having a piece of the action.

To be clear, this is not a knock on Elon. As an innovator and (perhaps more so) an operator, he certainly deserves a premium, but to this degree?

(Quick aside – while we appreciate that nuance, reasoned/balanced opinions, and middle-ground are relics of the 20st century (sigh), you really don’t have to be in either the “everything Elon touches turns to gold” or the “Elon’s a sham” camps. Seriously, this is not required. You’re allowed to see the good and the bad. Both are right there in front of you and (if you ask us) you do not do yourself much credit by planting your flag at either extreme.)

To quickly illustrate this point:

The Good: Tesla

The Great: SpaceX — an objectively incredible achievement in all respects, having literally turned outer space into a viable green space for all manner of commercial enterprises (honestly, it’s hard to overstate how audacious and impressive an achievement this company has been).

The Mid (as the kids say): The Boring Company — essentially a glorified construction company, that for some reason also makes flamethrowers.

The Bad: Twitter/X — an unmitigated disaster, to the point where Musk had to jam xAI investors with it to avoid being foreclosed on by creditors.

The Undetermined: xAI — It has certainly had a choppy start, with next to no revenue, an almost unfathomable burn rate, and a product that appears to be quite a ways behind the OpenAIs and Anthropics of the world. But at this point, it’s also far too early to really have much of any idea of how the LLM race will shake out (speaking of xAI and jamming companies with cashflow problems into companies with burnable cash, though, while we’re not sure we buy this prediction, it’s an interesting read nonetheless).

Getting back to our point here, would Tesla looking more and more like just a top tier automaker have put the Elon premium at risk? Probably. Will the recently announced abrupt pivots into robotaxis and humanoid robots (explicitly at the expense of the EV business) solve that problem? Even if it means a combination of a lot of new spending and further stagnation of the auto business that significantly reduces profitability?

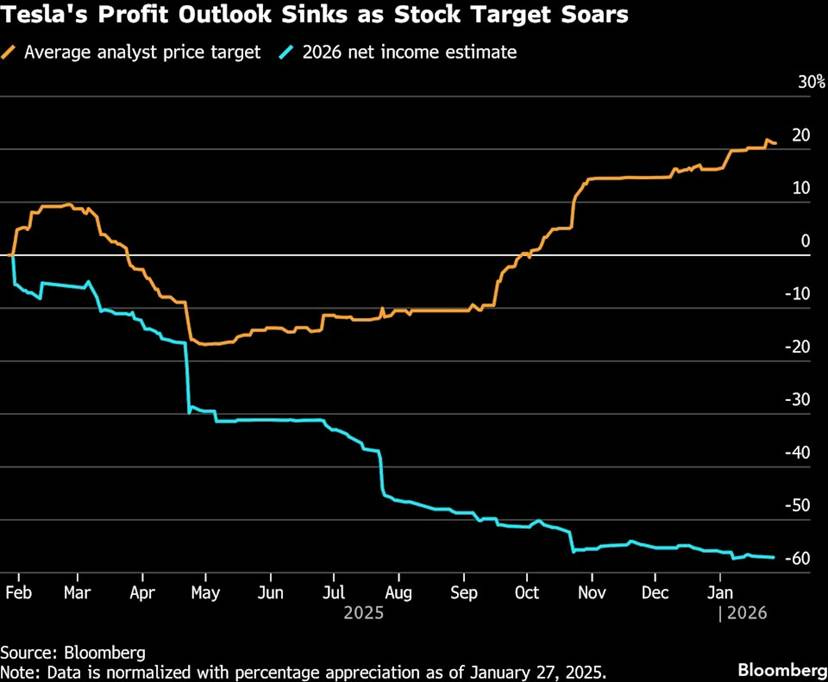

Well, Tesla’s Wall Street analysts’ 2026 projections (courtesy of Bloomberg) would suggest (at least for now) that it will, and then some (this degree of divergence between earnings and price projections is certainly not something you see every day):

While preserving Tesla’s premium valuation isn’t trivial (Toyota’s multiples applied to Tesla’s financials would result in a ~95% drop in Tesla’s stock price), to us, the more interesting questions are:

Is the big pivot really the best thing for the company long-term or just a hastily applied stock price Band-Aid?

Was there a better way to thread this needle without assuming the risk of a wholesale pivot and potentially squandering years of work building a huge lead in the EV space?

We’ll leave the humanoid robot aside for now. Tackling that is way too much of a digression, even for us, but this is an interesting, related take on the current hype-to-functionality ratio of various new products that’s definitely worth a read.

Focusing on the robotaxi business, while Waymo is certainly not going to have a permanent monopoly in the space, how realistic is it to think a viable competitor will pop up overnight (or even over a couple years’ worth of nights)? Initial reports of Tesla’s robotaxi progress in Austin are mixed at best and certainly give off a general air of something that’s been hastily slapped together to back up unrealistic promises (we would also highly recommend checking the source of any “reporting” here, as there are a couple of breathless worshipers with large followings and no scruples who are behind the most glowing “news”).

That said, there’s no reason to think Tesla couldn’t get there eventually, but is aiming to build and operate that first real Waymo competitor from scratch the best way to leverage Tesla’s strengths?

They have the cars, they have the cash to invest (as long as they don’t buy xAI), and they have organically collected a huge amount of the exact type of data needed for training AV operating software. But this endeavor also requires a substantial reallocation of cash and personnel focus, not just to building, but ongoing operational support, so much so that the company has publicly acknowledged it will require stripping pretty much all investment out of its core auto manufacturing business.

On the one hand, it may very well pay off and maybe in five years xCab or whatever will be the market leader. On the other had, it might result in a middle-of-the-road player in a highly competitive robotaxi market, sitting alongside a deteriorating EV business that is being lapped by a slew of new and rapidly growing competition from both traditional automakers and startup pure-plays (Rivian, Lucid, etc).

Most importantly, though (to us anyway), it seems like a waste of Tesla’s incredibly valuable brand and best-in-class manufacturing operation, both of which took years to develop.

While we appreciate that the old adage, “If you can’t beat ‘em, join ‘em” is anathema to 50 years of startup ethos, leaning into a company’s (and founder’s) strengths is also a core pillar of that ethos. What if instead, Tesla could take advantage of this new self-driving taxi phenomenon by leaning into its strengths, rather than kicking them to the curb in a wholesale pivot?

Tesla is world class at two things, efficiently building high-quality cars that people want to ride in and collecting data on every movement of those cars. As it happens, two of the three primary things robotaxi companies need in order to build, operate, and scale their businesses are cars and driver data. Is it too simple to suggest that they just partner with Waymo (or any other current or future competitor) to provide cars and training data?

From where we’re sitting, this has a huge amount of upside, potentially more than the pivot, since this would also enhance the core auto business, not kill it. It would also require minimal additional spending (and substantially all of that would be accretive to the core business anyway) and would produce immediate, high-margin returns.

In other words, follow the lead of the company that leaned into its strengths to provide the third thing that robotaxi companies need – software to manage the scheduling, routing, and rider interfaces.

We’ll get to that, but speaking of Waymo…

Is Waymo Actually Underrated?

Sixteen years, mountains of data injested, and countless hours of training and testing after its inception as a highly speculative and ambitious project within Google, Waymo delivered 14 million driverless rides to customers in 5 cities in 2025, three times the prior year’s total, and infinity times the number of autonomous rides in the entirety of human history up until 2015.

Even as recently as 20 years ago, this was the stuff of science fiction. It is a truly extraordinary milestone in human innovation, arguably even one of the top 10 or 20 ever and yet, the response seems to have been a collective shrug.

Shouldn’t we all be much, much more excited about this? Is the relative malaise a product of how long we’ve been hearing about self-driving, and/or the number of grandiose predictions around it that fell flat (none of which actually came from Waymo, incidentally)? Are we all just numb from the onslaught of content we’re now subjected to on a daily basis?

Who knows, but Waymo, consider us awed by this achievement. It is truly exceptional. You may take a bow at your leisure.

Now, whether Waymo’s rumored $100 billion fundraising round valuation is a shrewd investment, well, we won’t belabor this one, having written extensively about the perils of insisting valuations don’t matter. Suffice it to say, a company’s potential upside stops mattering the minute you decide to pay for all of that upside upfront, and this projected hundred-billion-dollar valuation is 40x the revenue these same folks are projecting Waymo will generate 5 years from now. Do with that what you will.

Speaking of Waymo, leaning into strengths… and Uber…

Is Uber in the Early Stages of a Future Business School Case Study on Adapting to Competition

Robotaxis pose no bigger threat to anyone than they do to Uber (and Lyft). A competitive service that takes in 100% of the fares it collects rather than 25-30% will, at scale, be virtually impossible to compete with. Faced with this reality, Uber could have gone full-Tesla and thrown everything into trying to rapidly piece together a competitive product (and it seems they considered doing just that for a time).

Instead, realizing that one of the major parts of a successful robotaxi business, the software for scheduling, routing, and interfacing with riders, happened to be their core strength, something they’ve already spent years building, testing, and refining, and into which robotaxi companies could seamlessly plug their cars, Uber has now inked partnerships with Waymo and other self-driving car companies.

So, instead of spending billions scrambling to put a competitive product on the road, essentially pivoting the entire business to something that may or may not even succeed, or simply watching their business slowly erode, they will maintain their core business, avoid a huge self-imposed cash crunch, and profit handsomely from the growth of this market right alongside the companies that could have been their undoing.

Future MBA candidates, when we see you out in the field, please just remember who gave you the head start.

Last but not least (pun absolutely intended)…

Is Apple Really Striking Out on AI or Are They Potentially the Smartest People in the Room?

Big grain of salt with this one as we have no inside information nor have seen a word about this in open source (i.e., this is pure speculation)… but is it possible that Apple isn’t woefully behind, missing the boat on, and/or in AI-denial, as most of the commentariat seems to think? That instead, they see the same bubble we (and many others) see and (unlike most others), are patiently waiting for it to collapse so that they can then scoop up the best companies/assets at pennies on the dollar?

We have touched on the growing AI bubble a few times in the past year or two, but to reiterate, the bubble is not about the technology itself, it’s about the prices being paid (and to some extent, how indiscriminate the choice of products has been). To be very clear on this, we have no doubt whatsoever that this technology will be at least as transformative as the rise of the internet was 30 years ago (perhaps significantly more so). But much like that early internet fever, we believe this AI craze has gotten far too hot, far too fast, and a substantial reset is coming (and is, frankly, necessary).

We have also previously written that, just like in the post dotcom bubble, we believe anyone with cash to spend will see their patience rewarded, not only in getting to buy great assets at distressed prices, but also in getting additional insight on the viability and demand for different products (and different versions of products) based on what survives the initial shock and what immediately disappears when funding stops being infinite.

Is it possible that the leadership at Apple simply remember those who waited for others to pour billions into Global Crossing’s infrastructure buildout (all the way up to a $50 billion peak market cap), were eventually able to reap the benefit of those assets at a 94% discount? Or those who waited for Amazon to decline, coincidentally, also 94% from its peak, saw their investment increase more than 500x over the next 20 years? Or those who watched Pets.com crash, had their initial reservations confirmed, and never gave it another thought?

Again, this is pure speculation, but in its 40+ years, Apple hasn’t really ever missed the boat on the potential of a new technology (more often, in fact, they’ve been the boat), so it seems unlikely to us that they’re just letting the potential of AI pass them by either. Just food for thought.

Chris caught up with two of C2V’s earliest founders — Cameron Hendrix of Magellan AI and Shilp Agarwal of Blutag (both 2019 vintage). Great people, strong products, and the steady, high-integrity execution we love to see.

Joined by analyst Jamie Redington, and a big thanks to Charlie Stephens at Fidelity Private Shares for convening the group. This is what the C2V community is all about.

Always great to see our 2026 tech predictions picked up by AlleyWatch.

Huge thanks to the team at Relevanz Public Relations and Steve Stratz for helping get this in front of a broader audience.

This is our 8th year publishing predictions, and we try to keep the scorecard honest — sometimes we get it right, sometimes we miss — but the goal is always to call things as we see them, not where the hype wants them to be.

Acquisitions Are Back, But Exit Math Still Matters

Chris is seeing signs that M&A is loosening up in 2026, pointing to Capital One’s acquisition of Brex as a signal that large strategic deals (and broader PE activity) are starting to return. He also flags a common misconception: headline exits don’t automatically mean everyone “won” — when prior private valuations were much higher, some late-stage investors can end up with little or no upside. The takeaway: the cleanest return potential is often built early-stage, where ownership and exit math can actually work.

Impilo Doubles Operational Capacity with New Warehouses in Philadelphia and Phoenix

Impilo announced major warehouse expansions in Philadelphia, PA and Phoenix, AZ to support rising demand and long-term healthcare partnerships. The new facilities will roughly double operational capacity, improving inventory management and distribution efficiency across a broader geographic footprint. The Phoenix warehouse is already operational, the Philadelphia site is expected to be fully online in Q1 2026, and the company plans additional expansions later in 2026.

WATS Sweepstakes Offers 12 Months of Free TRUE Waste Data Processing for One Facility

WATS is running a sweepstakes for North America–based facilities pursuing TRUE precertification, certification, or recertification by the end of Q3 2026, offering one winner 12 free months of waste-data processing for a single site. Eligible applicants must be actively managing 4+ waste streams and have a TRUE reporting cycle beginning August 2025 or later. Applications are open Dec 5, 2025–Jan 23, 2026, with the winner notified by email by Feb 27, 2026.

Gripp Rendezvoo Wins 2026 AE50 for Its New “Equipment Relationship Management” Platform

Gripp announced that Rendezvoo, billed as the first Equipment Relationship Management (ERM) platform, has been named a 2026 AE50 Award winner. The product focuses on the equipment asset as the organizing “source of truth,” helping OEMs, dealers, and operators align on the same timeline to resolve breakdowns faster and keep preventive maintenance on track. Rendezvoo combines real-time repair status, maintenance plans/reminders, in-conversation access to manuals/parts info, centralized communication, and field-to-factory insights to improve service outcomes across mixed fleets.

BriefCatch Raises $6M Series A to Expand AI Products and Pursue Disciplined M&A

Legal writing platform BriefCatch raised a $6M Series A led by Full In Partners, citing strong momentum including 126% net enterprise revenue retention and growing adoption across major law firms and courts (nearly 60 AmLaw 200 firms and many state/federal courts). The company plans to use the funding to accelerate AI product development and a targeted acquisition strategy, with the long-term goal of building a single, Word-native AI platform for elite legal writing, editing, and research. Founder/CEO Ross Guberman said Full In stood out for quickly understanding the technical roadmap and vision, and noted recent launches like AI-driven citation correction and a context-aware writing advisor.

Boostr + Passendo Partner to Centralize Newsletter and Email Ad Operations for Publishers

Boostr announced a strategic partnership and integration with Passendo to help publishers manage, forecast, and execute high-value newsletter/email ad campaigns directly inside the Boostr platform. The joint solution aims to give revenue teams a single source of truth by centralizing inventory, streamlining workflows across Sales/Ad Ops/Rev Ops, and feeding accurate performance and revenue reporting from Passendo into Boostr. The integration is available immediately to joint customers, positioning email as a more scalable, trackable, high-margin channel alongside display and native.