C2V March Notes From The Trenches

Welcome friends! Well, despite being right in the middle of March Madness, we decided to go entirely the other direction and dive into the what and why of our core investment thesis this month (which as most of you know, will never have “madness” anywhere near its description).

Some of you long time readers may vaguely remember our having done this once before, but it’s been close to three years (and a few thousand new readers) since then, so we figured it was worth a refresh. Plus, quite a bit has happened in that intervening time: the macro trends that partly informed our original decision have actually gotten more supportive, the thesis seems to be working (lots of companies added in those three years that are doing extremely well, and for the reasons we thought they would, which is nice), and while we were pretty sure we were doing the right thing at the time by sticking with boring-but-steady despite quite a lot of buzz over some hot-but-definitely-a-little-suspect options, we now know for sure (though we’re still waiting for Meta to change their name back).

All that and a new portfolio company that we’re excited about despite it being all over Matt’s corner (named Alivo, also from Maine… it’s definitely a little awkward, but we’re working through it).

But first, a quick trip into the decidedly mundane (but at the same time, enthralling?) world of old-economy productivity tools.

Automating the…

It would be an oversimplification to try and lump VCs into two, three, or even twenty different buckets, but for illustrative purposes, we’ll look at our thesis as compared to arguably the biggest (or at least the most recognizable) of these buckets, which also happens to be the polar opposite of ours. We’ll call this the “Shiny New Toy” strategy (or “SNT”).

Anyone who has ever thought being a VC sounded cool was almost certainly picturing a SNT fund — being in on the ground floor of the next consumer-facing household name (Uber, Spotify, Rivian, etc.) or some brand new tech that becomes the next big breakthrough (one of the companies mining asteroids, training an LLM, building a nuclear fusion reactor, etc.). Could be some other version of this, but whatever they were picturing definitely did not include, for example, SaaS that tracks garbage collection and disposal.

So why did our venture dreams take a sharp turn away from all the cool stuff and make a b-line for the world of freight hauling, waste management, utility maintenance, plating & coating manufacturers, etc.? Glad you asked.

Why This?

There are several reasons (in no particular order):

A one-step sales process

As one of our esteemed, OG (first fund, first close) LPs once put it, a SNT founder aims to build the world’s coolest hammer and then go looking for nails, while our founders get so tired of they and their coworkers being hindered by the same loose nails day after day, they eventually get fed up enough to quit that job and build a hammer for it.

What this means in practice is that before a SNT founder even starts selling their product as the solution to a particular customer problem, they have convince the customer that the problem even exists in the first place.

This isn’t impossible, of course (circa 2010, people who really wished they had access to a ridesharing service was pretty close to zero; today, people who are willing to live without Uber is pretty close to zero), but it significantly increases the degree of difficulty for something that isn’t especially easy to begin with (i.e., for every Uber, there are hundreds of products that it turns out no one actually does want).

On the other hand, when a DDD founder walks into a sales meeting, everyone in the room is already well aware of the problem(s) that founder is addressing (often it’s the bane of that potential customer's professional existence), the DDD founder just needs show that their product will solve it.

Clear, Immediate, & Quantifiable ROI (or, Products That Sell Themselves)

Because the customer is already well aware of the problem(s) a DDD product is built to solve, they’re also aware (at least ballpark) of the cost of that problem, and therefore can immediately appreciate both the scale of the products’ potential ROI and the immediacy with which that ROI can start to accrue.

This not only improves the speed and success rate of initial sales, it also does the same for long-term retention (as once customers have seen the better way of doing things, they generally have zero interest in going back).

Huge TAMs & Essential Industries

These old-economy sectors generally start at “massive” and only get bigger from there. In most cases, SaaS companies can hit 9-digit revenue levels without cracking 1% market share. The upside is, for all intents and purposes, unlimited.

These sectors have also been around for decades (if not centuries), have been through dozens of market cycles, and are essential to the US and global economies. In other words, they aren’t going anywhere, almost regardless of what happens on a macro level. Web3 might be a considerably more exciting space than, say, medical imaging, but if we’re in a recession and you have to cut something from your budget, is it your crypto monkey NFT or your kid’s x-ray?

In addition, the nature of these products themselves make them in some ways more appealing in an economic downturn, as they are specifically built to allow companies to do more with less.

The Entire US Economy Needs This; Badly

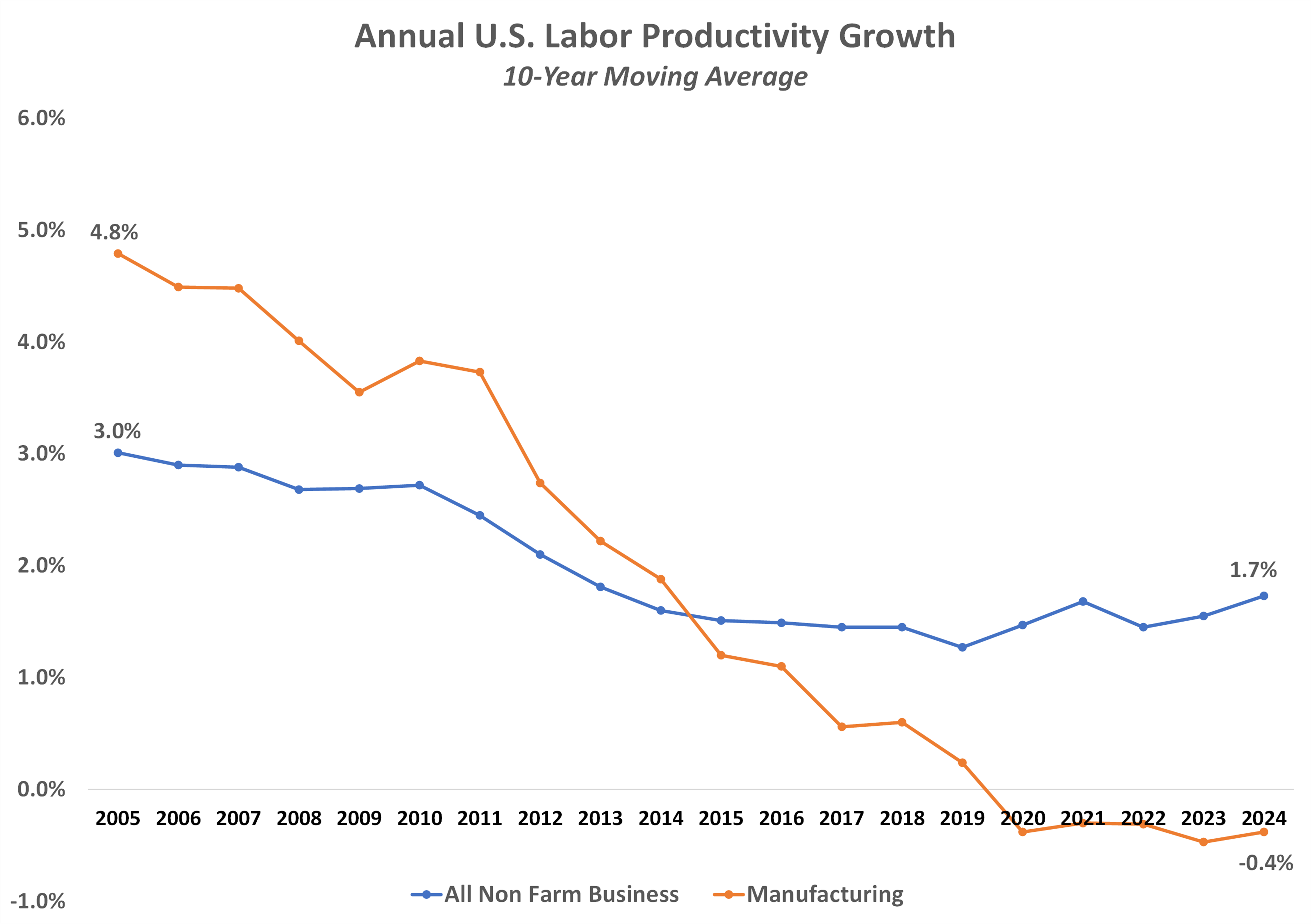

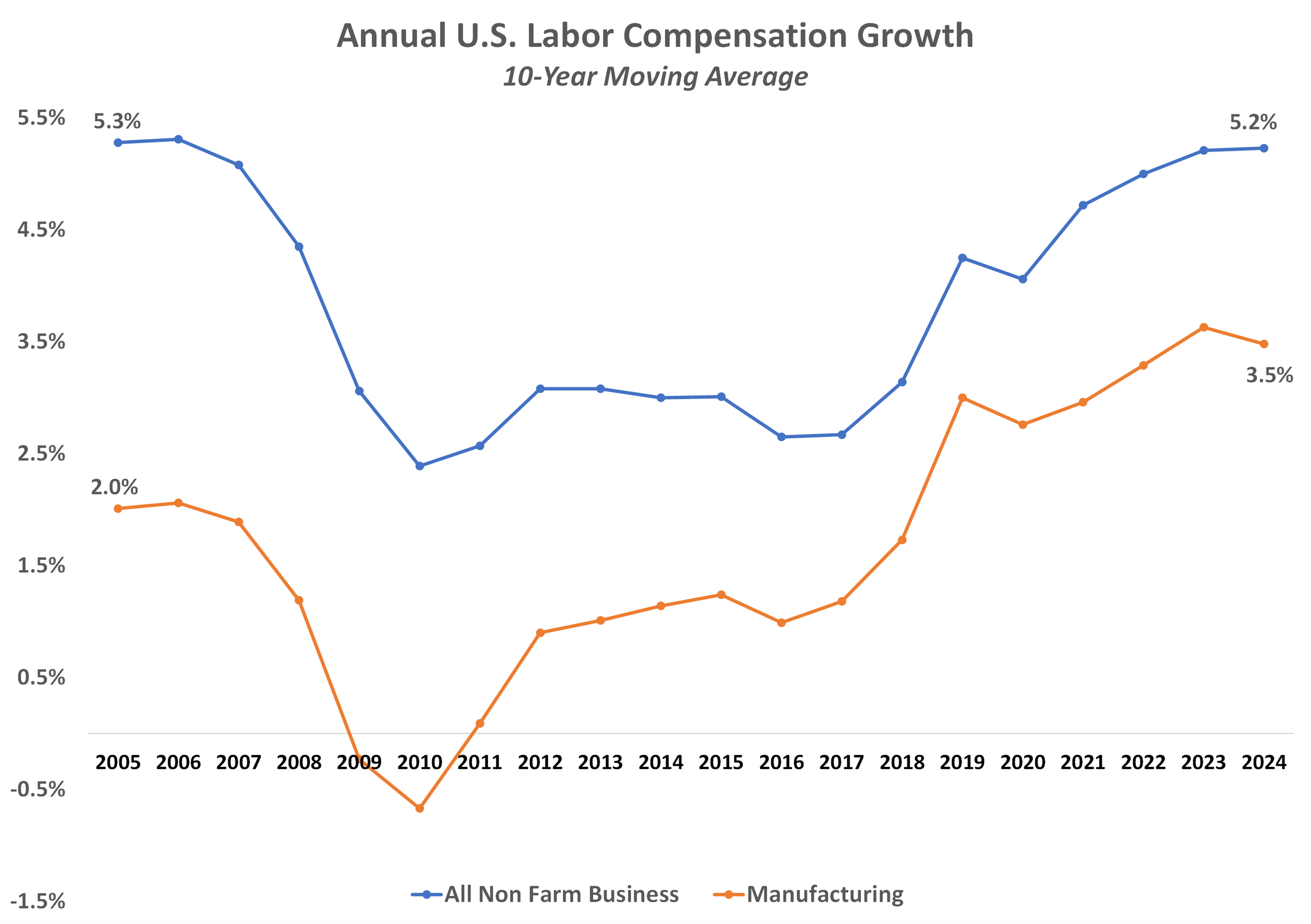

Annual productivity growth, once a hallmark of the US economy, is now approaching the end of its second decade of nearly uninterrupted decline. On top of this, several major structural trends that were more or less productivity-neutral during much of this time are now actively working against it to a steadily increasing degree. We’re certainly not economists, but from where we’re sitting, there’s no halting this decline (never mind seeing a rebound) without massive (and we mean, massive) new tech investment across just about every major sector (on a related note: the answer to “how do your target customers do this today?” from two different companies we talked to just this week was “by fax”, so there’s plenty of green space here).

Annual productivity growth for all Non-Farm Businesses (government speak for “more or less the whole economy”) seems to have at least stopped declining (for now, anyway), but still sits around half what it was 20 years ago. Meanwhile manufacturing continues to crater, now having seen negative productivity changes in 5 of the past 10 years, plus another 3 that were essentially flat.

In fact, since the 2008 financial crisis, annual manufacturing productivity growth has averaged 0.25% (vs. +3.5% a year in the 20 prior years, including 2008).

You’ll find a similar story, pretty much across the board.

For example, the five industries below that we definitely selected at random and not because they’re buying software from C2V portfolio companies like, say, Medmo, Digital Iron, Steelhead, Driver Tech, and Noteworthy...

Improving Jobs & Replacing Openings

Contrary to popular belief, almost none of these productivity-enhancing automation products are replacing jobs. On the software front, they’re generally improving jobs, allowing overworked employees to do more with less, while taking away their least-rewarding, most mind-numbing tasks. There are even some studies out there (of both the probably-unbiased and grain-of-salt varieties), based on worker surveys, showing that automation generally has a positive impact on job satisfaction.

Even those robotics platforms that may do all or nearly all of the tasks of what would traditionally have been a full-time human role are generally not replacing jobs; they’re replacing perpetual job openings, a relatively underappreciated and increasingly problematic phenomena of the past 15 – 20 years.

Obviously, there is some natural ebb and flow with economic cycles and more recently, some Covid-related noise, but even accounting for shorter-term volatility there remains a very clear long-term trend. In fact, the smoothed trend line has increased at roughly 5.1% per year since 2003 (2.8x overall), accelerating to 6.6% annually over the past decade. This despite current unemployment rates sitting just above 70-year lows, and a 17% increase in the working age population over this time period. In fact, job openings as a share of working age population have increased from 1.7% to 4.1% over the past 20 years.

Some of this is due to a shortage of qualified candidates for high-skill positions, but the lion’s share are jobs that Americans simply don’t want, because they are too… wait for it… dirty, dull, or dangerous.

(Either that or we've become a nation of hopelessly lazy, selfish, entitled prima donnas. But at least we have robots?)

This has also had the secondary effect of pushing up wages, as some employers become increasingly desperate to fill these persistently open roles, which in turn further increases productivity headwinds.

So yes, building and selling a novel software or robotics product is still among the harder things you can set out to do in your career, but we would continue to argue that focusing on a glaring customer need that’s often bordering on desperation and isn’t going away anytime soon lowers that degree of difficulty about as much as it can be lowered.

As a last note on this, we offer a quick salute to the unwavering discipline of our founders in sticking with the practical over the splashy. It’s not easy for a talented, bright, creative entrepreneur to resist the allure of the SNT ethos, even after they’ve chosen to swim in the automation-of-the-mundane pool. Take, for example, some of companies we’ve recently seen showing off humanoid robot prototypes for commercial/industrial automation applications.

They may look cool, but it’s hard to more perfectly miss the entire point of robotics. If the goal is to build something that performs tasks for which humans are most poorly suited, why would you start with a replica of a human? Given that these folks are plenty smart enough to know better, we’d hazard a guess that it’s because the press and public will be far more enthralled by something that looks like this (a shiny new toy):

Than by something that looks like this (a super sophisticated software suite, wrapped in a Dr. Seuss machine):

It may not be pretty, but it can do all of this (fully autonomously), which is ultimately the only thing that actually matters.

We’re pleased to announce our latest in investment in Alivo, from our pre-seed, Tributary Fund. Alivo’s custom AI agents act as a seamless 24/7 virtual customer support and sales team for home service businesses, handling inbound calls, follow-ups, and appointment bookings.

In a business where sales leads are dominated by third-party platforms who will sell each lead to multiple providers simultaneously, delays of even a few minutes in responding to new leads can drop close rates to near zero. With 24/7 human coverage simply not a realistic option for service providers, Alivo’s ability to fully automate the entire lead responses and follow-up sales process is a massive advantage for its customers, often resulting in an immediate 30-50% uptick in monthly sales.

By The Numbers

Dirty, Dull, and Dangerous

Chris offers his perspective on our thesis sweet spot: where legacy meets opportunity. Dirty, dull, dangerous, and ripe for reinvention.

Developing Intuitive Agtech with Gripp CEO Tracey Wiedmeyer

In an interview on Agency29's blog, Gripp CEO Tracey Wiedmeyer discusses the development of intuitive agricultural technology (AgTech). He emphasizes the importance of creating user-friendly solutions that address the specific needs of farmers and agricultural professionals. Wiedmeyer also highlights the role of data analytics in enhancing decision-making processes within the agricultural sector. Additionally, he shares insights into Gripp's approach to innovation and their commitment to improving efficiency and productivity in agriculture.

BriefCatch 4 Launches with Revolutionary AI Bluebook Citation Tech and an AI Advice-and-Examples Chatbot

BriefCatch has launched BriefCatch 4, introducing groundbreaking AI features for legal writing. The update includes an AI-powered Bluebook citation tool that automates legal citation formatting, enhancing accuracy and efficiency. Additionally, it offers an AI advice-and-examples chatbot, providing users with tailored writing guidance and examples. These innovations aim to streamline legal writing processes and improve document quality.

Tarform Wins 2025 iF Design Award

The Tarform Luna EV Motorcycle, winner of the iF DESIGN AWARD 2025, seamlessly fuses art, craftsmanship, and technology into a striking electric ride. Designed with a modular approach for lasting durability, it redefines sustainability by challenging mass consumption in favor of longevity. Tarform is dedicated to zero-emission manufacturing, integrating cutting-edge technology with ecological responsibility to move towards a zero-waste future. Every element is thoughtfully crafted to celebrate the essence of motorcycling while embracing the evolution of modern mobility.

The most innovative companies in enterprise for 2025

Fast Company highlights the most innovative enterprise companies of 2025, with AI playing a central role in many of their advancements. Companies like UptimeHealth ensure that medical, dental, and veterinary practices keep their equipment running smoothly. In 2024, it launched a medical equipment management system integrating various devices to predict maintenance needs and prevent downtime. The system, liken to Google Home for medical practices, uses IoT technology to collect equipment data and automatically dispatch technicians or guide staff through simple fixes. The company grew rapidly, increasing revenue from $1M in 2023 to an expected $10M in 2024, expanding to over 6,000 locations. UptimeHealth also acquired Dental Whale and partnered with Darby Dental Supply to enhance its service offerings.

Future Food-Tech Summit

Wats attended the Future Food-Tech meeting with industry leaders, hearing fresh perspectives and diving into the challenges facing food manufacturers today. One theme stood out: waste isn’t just waste—it’s a resource. Companies are eager to turn byproducts into valuable inputs.