C2V October Notes From The Trenches

Welcome friends! This is normally the part of the newsletter where we’d have some fun with something topical that made us chuckle (even better if that thing was very clearly not meant to be funny) and this truly off-the-rails election season just keeps throwing us red meat on what seems like an hourly basis... but this is also about as hyper-charged a lightning-rod political environment as we can remember and it… well… it's turned us into abject cowards. There, we said it.

So, with apologies to those of you who might have been looking forward to the usual antics, we’ve relegated all election content to the C2V vault to live out its days next to pictures of Chris’s tattoo and every haircut Matt had from ages 5 to 24.

We promise to be back to normal next month, but in the meantime, our quarterly deep dive into the macro venture data unearthed some early signs of an extremely encouraging new trend that we think will have near universal approval, so don’t go anywhere just yet.

Exit-Gate

In an industry that seems to do a lot of handwringing in general, it’s notable just how wrung hands have gotten over the state of venture-backed exits over the past 2.5 (post-bubble) years. The headlines below (the result of 2 minutes of googling just now) are just a drop in the bucket for the amount of press that this topic has received over this time period, and you can multiply the press coverage by at least ten before you’re anywhere near the number of times we’ve heard folks grumble about what a barren wasteland of tech startup demand we’ve all been saddled with.

But as we dig into recent macro data, it’s hard not wonder if there is a whiff of gaslighting here (not from the press, but from those who feed them stories), perhaps in an attempt to deflect or at least defer some blame for the state of those late-stage portfolios who should be seeing consistent exits (sold as they were on a pitch along the lines of “venture returns in half the time”), but have spent the past 2.5 years largely sitting on a whole lot of positions they can’t or don’t want to sell at market clearing prices.

Let’s start with some recent data from the good folks at Pitchbook and the NVCA.

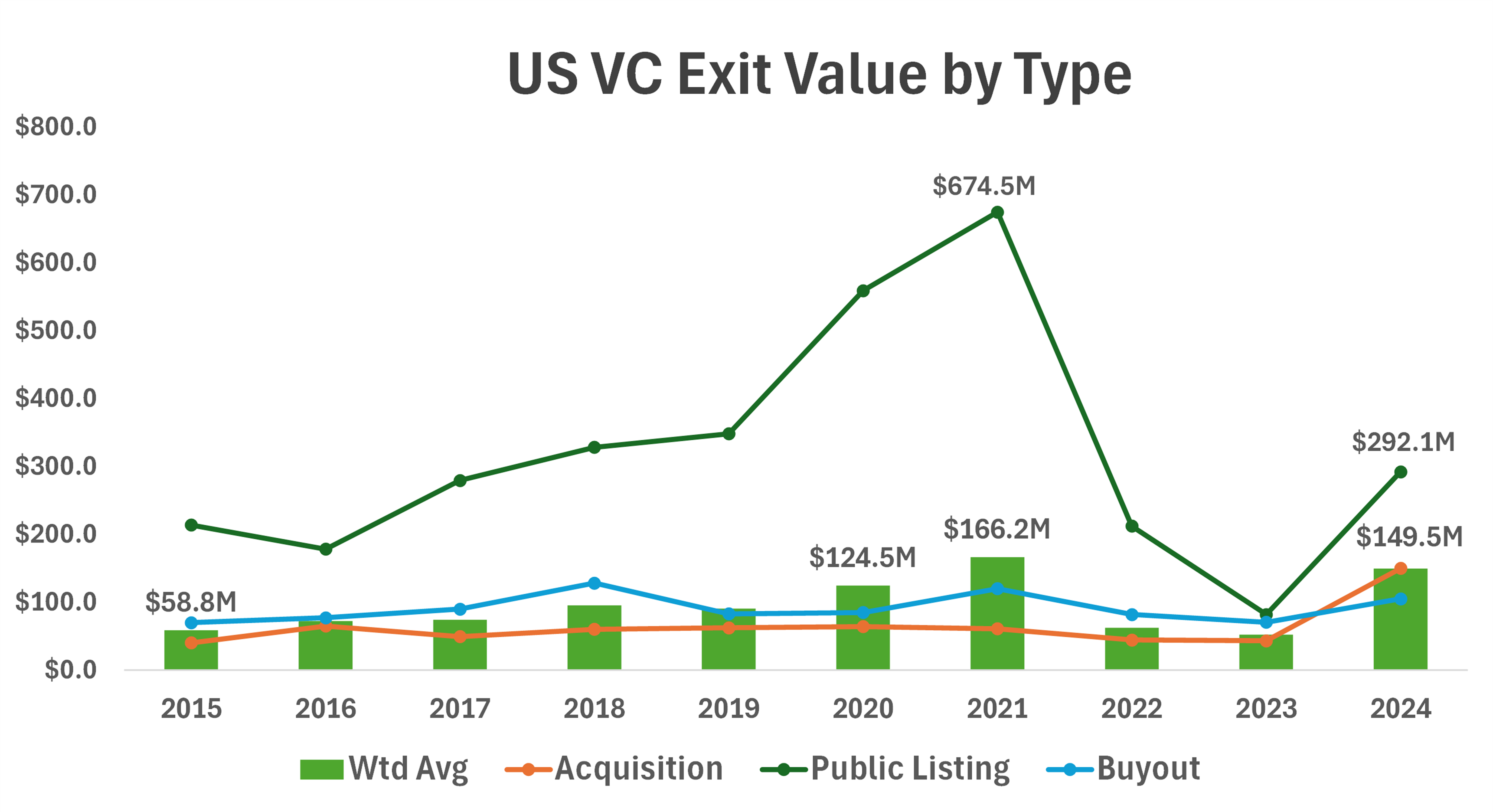

While the total number of exits remains roughly flat from the prior two (post-bubble) years, the value of these exits is now on pace to be 3.5x higher than last year and the third highest in the past 12 years, behind only 2021 (a crazy outlier year that may not be topped for another decade or two) and 2020 (just 16% higher than this year’s pace). This is particularly extraordinary given that we also remain at the lowest share of exits with values disclosed on record, and less than half the share disclosed in 2020 and 2021.

The driver here is the median exit value, which, at $149.5 million, is nearly triple last year’s and just 10% lower than the aforementioned crazy outlier 2021 number ($166.2 million). This too is an exceptional data point, given what would ordinarily be an unfavorable mix of exit types thus far in 2024.

Typically, median public listing values are far higher than those for corporate M&A or PE buyout exits, and as a result, years with the largest median exit values overall generally have a large proportion of public listings relative to M&A and buyouts. For example, the only other years with an overall median exit value north of $100 million (2020 and 2021) were years in which public listings accounted for 71% and 84%, respectively, of exits with disclosed values.

This year, that number is only 47%, and the median public listing, while still quite healthy relative the prior years, is only 2.1x the median of the other exit types (vs, for example, 9.0x in 2021). The difference is that we’re seeing exceptional strength in PE buyout ($105 million, behind only 2021) and M&A valuations ($150 million, 2.3x the second-highest year on record).

What This (Probably) Means

We’re entering the realm of speculation here, so grain of salt, but what this looks like to us is a market with very, very strong demand for strategic (M&A) and financial (PE buyout) acquisitions of VC-backed tech startups and perhaps some supply limitations as well. There’s really no other way to explain the historically high valuations being paid by these buyers.

We also suspect that the IPO market is not nearly as closed off as the prevailing narrative would have us believe, but rather, this is just a story being spun to explain the sudden and persistent drop off in liquidity in late-stage funds from 2021 to today:

Not only are U.S. public equity markets currently at all-time highs, but they’ve gone nearly straight up for the past 22 months. It’s possible that past market tops also featured “closed” IPO markets, but it seems incredibly unlikely, and we certainly haven’t seen such a situation over the past 12+ years. Furthermore, the 50% gain in the NASDAQ Composite over the past 18 months compares quite favorably to prior periods of heightened VC-backed IPO activity (e.g., 2013: +46%, 2014: +39%, and 2019: +17%).

Sure, SaaS revenue multiples are somewhat less favorable than in the past, currently trading at 6.1x ARR run rates vs. a longer-term average of 8 - 10x (per the SaaS Capital Index), but we believe this is more likely a function of the quality of the companies that make up the majority of the public SaaS sector than a function of the market overall:

As we noted in our public SaaS deep dive in our March 2023 newsletter, 80% of the companies in the index were unprofitable (most extremely so), with a full 60% of the index having snuck-in their IPOs between 2019 and 2021, when no one was paying attention to all of that useful information below the “revenue” line on income statements.

Profitable SaaS companies, even the big, relatively slower-growing ones (e.g., Adobe, Autodesk, Microsoft), are all generally trading well north of 10x revenues.

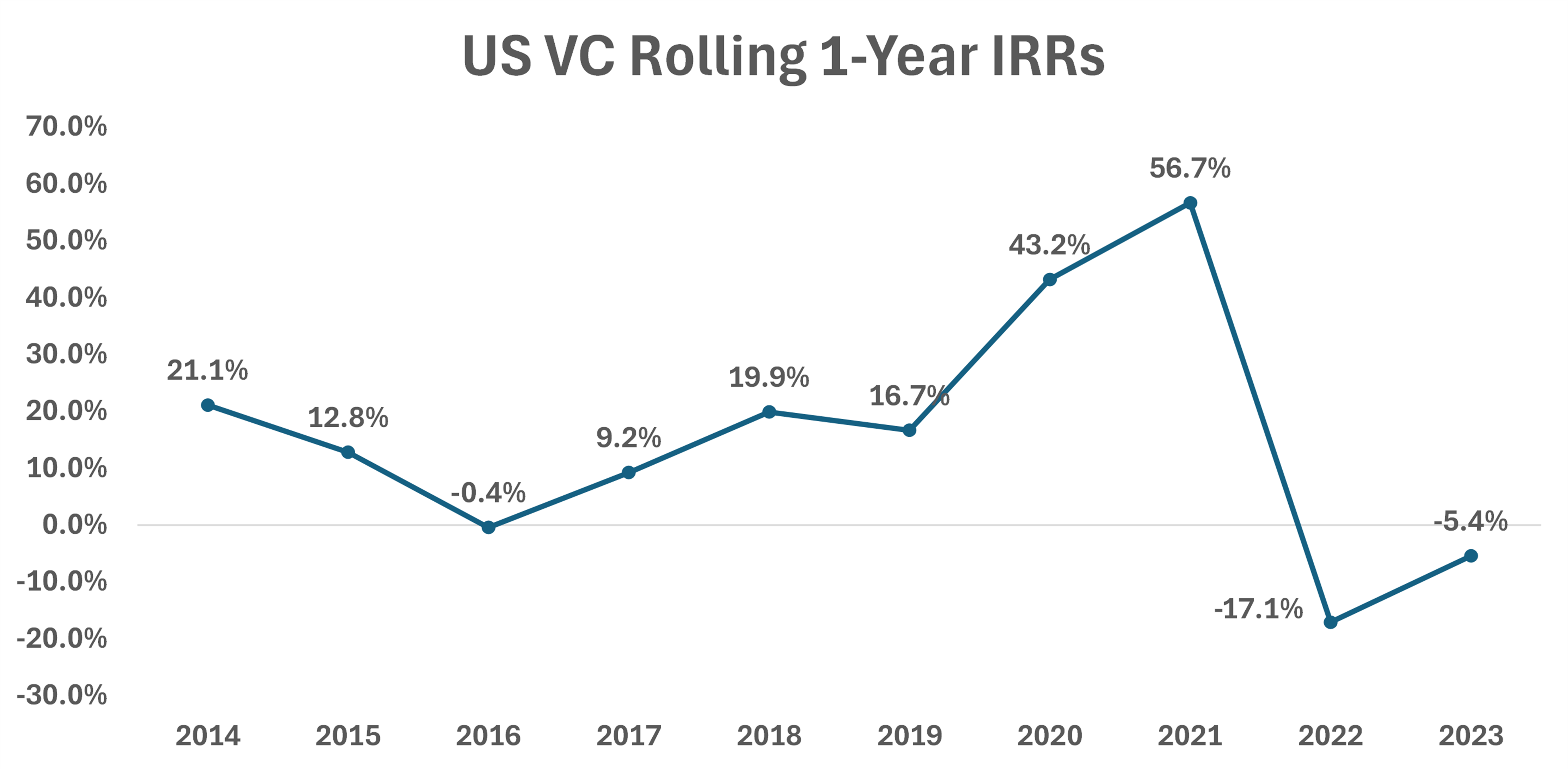

We actually suspect that the real issue is that funds either A) are reticent to expose late-stage companies to the scrutiny of a full IPO underwriting process, or B) don’t want them to IPO even if they could because they’re still massively underwater relative to 2020/2021/early-2022 valuations. Obviously, we’re speculating a bit here, but there is certainly plenty of evidence to suggest that late-stage portfolios are, in fact, in fairly dire shape, both in the Venture Monitor’s industry-aggregate IRR numbers and in secondary market activity over the past year or so:

Prior to 2022, the only period in the VM’s dataset (going back to 2014) with negative IRRs on a rolling 12-month basis was in 2016. That period spanned three calendar quarters when the industry averaged a -1.1% IRR. By contrast, the first quarter of this year (the VM reports IRR on a 6-month lag relative to other data) marks the 7th consecutive quarter of negative IRRs, for an aggregate decline since mid-2022 of 22% (for context, 2-year returns from 2014 - 2019 — pre-bubble — averaged +25.7%, with a low of +8.8%).

As bad as these IRR numbers are, they likely understate the magnitude of the issues with these seasoned, scaled companies that are supposed to have reached the sweet spot for exit. Secondary market data (which is both more objective and more timely than the VM’s funding-round-based IRRs) paints a considerably more stark picture. Of the 66 companies listed last week on secondary platform Hiive Markets, where the prior funding round valuation was known, the average company was trading at a 49% discount to that prior round, and only 4 were trading above where they last raised private capital (at a whopping 5.5% average premium).

Furthermore, this most recent data is quite consistent with what we’ve seen throughout the past 10 months. Of the 25 weeks of 2024 Hiive data we’ve looked at, the average discount to prior funding round has been 47.5% (in a range of -42.8% to -52.0%), and of the 517 companies with a known last funding round valuation who traded on the platform over this period, only 29 (5.6%) traded above their last funding round valuation at least once (29! Out of 517! Over 10 months!).

Bottom line: Don’t believe the doom-and-gloom venture exit market narratives; the buyers are there, and they’re willing to pay up for good companies. It looks to us like the issue is more with the quality and/or (unrealistic) price expectations of the companies at the exit stage.

C2V Watercooler

We've enjoyed connecting with prospective LPs, founders, partners, and friends from Jackson Hole to Milwaukee, Detroit, and Cincinnati.

The Midwest and Heartland America continue to be a focal point for our investment thesis—especially in B2B SaaS, Robotics, and industries often considered "dirty, dull, and dangerous."

These regions are home to incredible, often overlooked founders, and we’re excited to support them.

We also appreciate the fair valuation expectations, making these areas even more attractive for investment.

While CT/NY will always be home and our backyard we are excited to lean into these communities and look forward to sharing what’s next for C2V.

Portfolio Highlights

Does online search for groceries even work?

In this episode of #GroceryShop, the Middlemen explore how generative AI and conversational search transform grocery shopping by moving beyond basic keyword search. This technology shift, especially in meal planning, enables users to describe their needs and preferences for more intuitive results simply. They’re joined by Shilp Agarwal, CEO of Blutag (blu.ai), and Clive Humby, loyalty marketing pioneer and co-founder of DunnHumby, famously known for the phrase “Data is the new oil.” Together, they discuss the future of AI in eCommerce, followed by a demo of Blutag's platform at the end of the episode.

Magellan AI Adds New Geo-Targeting Feature

Magellan AI has introduced market-level reporting within its measurement dashboards, enabling advertisers to analyze regional ad performance quickly and optimize targeting strategies. The new feature allows users to generate insights directly within the app rather than through an API, enhancing geocentric campaign adjustments and ad spend efficiency. This addition aims to help advertisers better allocate spending to high-performing markets. As Chartable closes, Magellan AI is positioning itself as a strong alternative, demonstrating improved conversion tracking through recent case studies with clients like Wildgrain.

iHeart, Magellan AI launch new award to celebrate top podcast advertisers

ARN’s iHeart and Magellan AI have launched an initiative to recognize top investors in Australia’s podcast industry, awarding OMD Australia the inaugural "Australian Agency of the Quarter" for Q2 2024. The initiative also highlights the top podcast advertisers, led by BetterHelp, McDonald's, and Airbnb. Using AI, Magellan analyzes ad spend and placement across 400+ popular Australian podcasts, revealing increased investments in podcast advertising, particularly in Business and Comedy. This initiative aims to encourage further growth in podcast advertising by showcasing high-impact brand contributions.

How to Create a High-Performance Organization Through a Successful Merger

This article from Entrepreneur outlines best practices for integrating teams post-merger, emphasizing the importance of transparent communication, proactive leadership, and fostering unity. Jinesh Patel shares his experience merging UptimeHealth with Dental Whale, where open communication and adapting new systems eased the transition and built trust. Regular check-ins and transparent leadership were key to managing anxieties and aligning team goals. Patel’s approach illustrates that empathetic, transparent leadership creates smoother mergers and establishes a solid foundation for growth.

Eskuad will help those affected by the wildfires in North America.

“I experienced the same in 2023 when my dad and mom were the first responders when a wildfire got too close to a school and the building they live in, my dad being a volunteer firefighter and son of a firefighter himself,” said Max Echeverría.

Eskuad decided to make the pro version of its product available to the people and companies affected by wildfires, who must report to insurance or manage the restoration processes.

Please feel free to share this information with anyone who might need to collect data and streamline operations during the emergency, and do not hesitate to reach out to us if there is anything we can help with to make the most out of our platform in these hard times.